Edge Case

Testing AI products at the edges so founders don't have to.

This was a quick external test using the product’s free credits. I may be missing internal context, and I’m happy to correct anything if the team provides evidence.

Vouch API launched on Product Hunt this week claiming to offer institutional-grade AI equity research that “proves it isn’t lying.” The pitch includes citation coverage requirements, economic plausibility checks, and FINRA 17a-4 compliance stamps on every report.

I spent 30 minutes and 25 free credits stress testing it. I tested two non-standard but obvious ticker cases: a defunct U.S. company and a major foreign-listed company outside the SEC ingestion path. Both resulted in significant failures.

The results raise a question worth asking about any AI product making strong reliability claims: what happens at the edges?

Test 1: A Company That Has Been Bankrupt for 23 Years

The first test was simple. I entered ENRN, Enron’s ticker, into the system.

Enron filed for bankruptcy in December 2001 in what was then the largest corporate bankruptcy in US history. The company no longer exists as a normal operating public company. There are no current financials, no active SEC filings, no price, no shares outstanding.

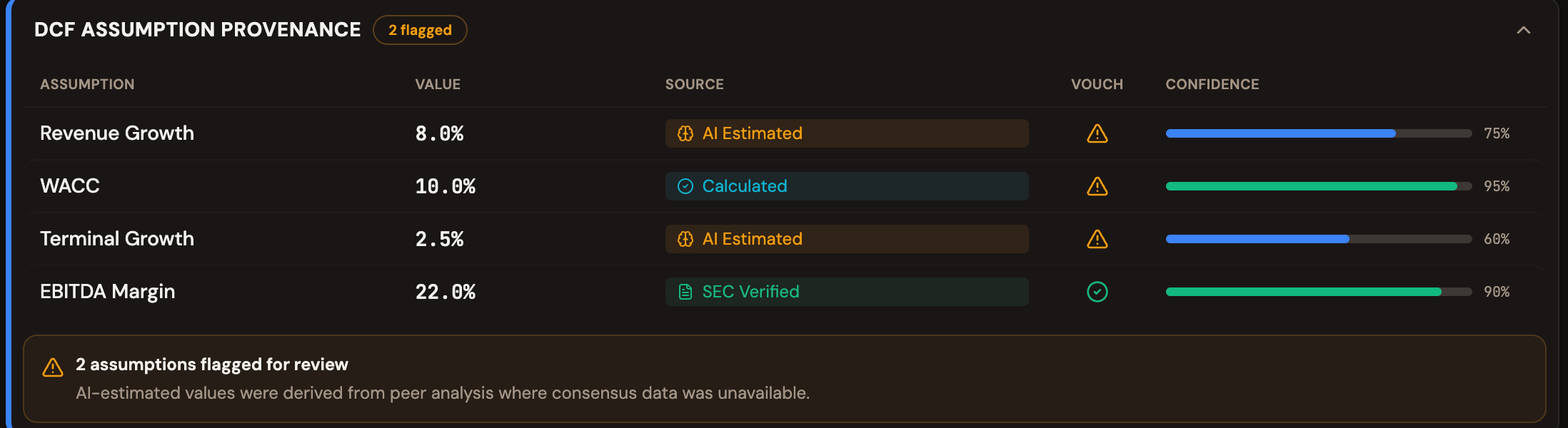

Vouch generated a full research report anyway.

The valuation failed, which is the correct outcome. But buried in the report was this: an EBITDA margin of 22.0%, sourced as “SEC Verified” with 90% confidence and a green checkmark.

This may be technically true in a narrow historical sense. Enron did file SEC documents before its collapse. The system may have retrieved historical SEC filings from before the bankruptcy and presented them as current verified data, with no indication of their age.

A user who didn’t already know Enron’s history would see a green checkmark, a specific number, and 90% confidence and have no reason to question it.

The report also left its investment thesis sentence literally incomplete: “At $0, ENRN .” The sentence ends there. A pipeline stage failed silently and the report was delivered anyway.

Test 2: A Company That Doesn’t File With the SEC

The second test was more revealing. I entered VOW3, Volkswagen’s Frankfurt Stock Exchange ticker.

Volkswagen is one of the largest automakers in the world. It is a real, actively traded company with billions in revenue. It is also a German company listed on the Frankfurt Stock Exchange, which means it does not file with the SEC and does not appear in EDGAR.

Vouch acknowledged this directly in the financials section: “No financial history available for VOW3. Data populates when SEC EDGAR ingestion runs for this ticker.”

While Volkswagen does file some documents with the SEC as a foreign private issuer, 13F institutional ownership data and Form 4 insider transactions are US-specific filings that do not exist for Frankfurt-listed shares.

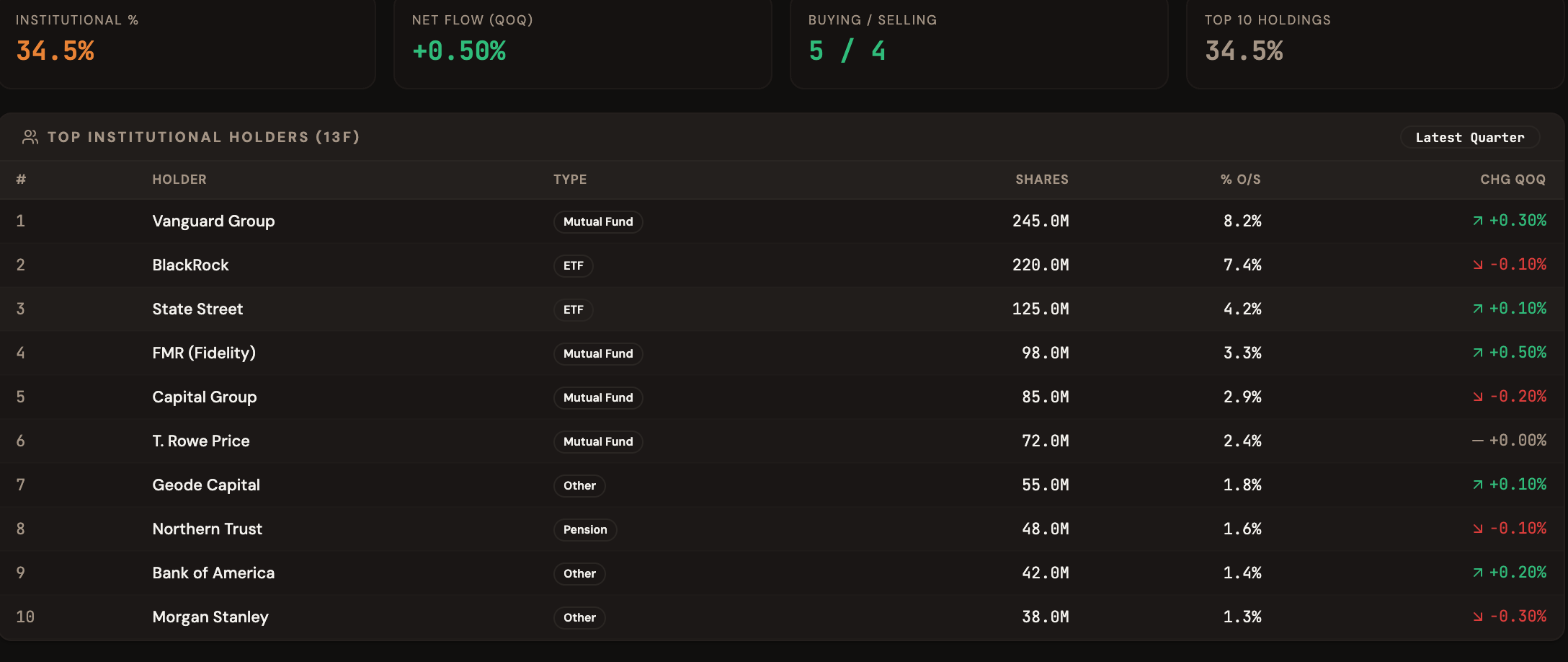

Then, in the same report, it generated a complete institutional ownership table.

Vanguard Group: 245 million shares, 8.2% ownership, up 0.30% quarter over quarter. BlackRock: 220 million shares, 7.4%. State Street, Fidelity, Capital Group, T. Rowe Price, Geode Capital, Northern Trust, Bank of America, Morgan Stanley. Ten institutions, specific share counts, specific percentages, specific quarterly changes.

A Frankfurt-listed ordinary share is not the kind of U.S. SEC 13F data source this report appeared to be imitating. I could not verify these figures from the relevant official sources, and the report itself had already stated that SEC data was unavailable for this ticker.

The report also generated specific insider transactions. A CEO selling 50,000 shares at $185.20 on February 15, 2026. A CFO buying 10,000 shares at $178.50 on January 28. A director exercising options at $145.00 on January 15.

I could not find evidence for these transactions in the expected official sources. They are invented with specific dates, prices, and quantities, formatted identically to real insider transaction data.

The system admitted it had no SEC data for this ticker. It then generated two pages of specific financial data anyway.

The Pattern

These two tests share a common failure mode that is worth naming clearly.

In both cases, the system encountered a data gap. Enron has no current financials because it does not exist. Volkswagen has no SEC data because it is not a US listed company. In both cases, the system filled that gap with something that looked like real data.

This is different from being wrong. A system that says “I don’t have reliable data for this ticker” is being honest about its limitations. A system that generates specific institutional ownership percentages and insider transaction prices when it has already told you it has no data is doing something more problematic. It is producing fabrications that are formatted, cited, and presented identically to real verified information.

The danger is not that the system fails. The danger is that it fails in a way that looks like success.

A non-technical user seeing a table of institutional holders with specific quarterly changes, or an EBITDA margin stamped SEC Verified with a green checkmark and 90% confidence, has no obvious reason to question it. The presentation is professional. The numbers are specific. The formatting is identical to what real data looks like.

Vouch’s core claim is that it proves it isn’t lying. These tests suggest the harder problem is not lying but not knowing when it is.

What This Means

Vouch is not uniquely flawed. The failures I found are representative of a broader problem with AI products that make strong reliability claims.

The vibe coded AI wave has produced hundreds of products that ship fast, look polished, and make confident claims about accuracy and trustworthiness. Most of them are not systematically tested beyond “it seems to work.” Edge cases, data gaps, and failure modes are discovered by users after launch, often in high stakes situations.

In fintech this matters more than most domains. A fabricated-looking institutional ownership table or an unverifiable insider transaction is not a harmless UI bug. It is the kind of output that could inform a real financial decision.

The two tests I ran took 30 minutes and cost nothing. They were not sophisticated attacks. I did not try to break the system. I asked it about a bankrupt company and a foreign stock, two scenarios any serious equity research tool should handle gracefully.

I am building a tool that automates this kind of stress testing. The goal is to catch failure modes like these before they reach users, not after. If you have an AI product and want it tested, reach out.

Hey love this, but one tthing worth noting is that international tickers are not yet available, if a report fails the outcome is correct, we are still early and refining the product and appreciate the things you have pointed out we will take a look into these.